In the rapidly evolving fintech landscape of 2026, the super.money ecosystem (backed by the Flipkart-Axis alliance) has disrupted the traditional credit market. While the standard SuperCard is to target the credit-starved users, the SuperCard Pro has emerged as the heavy-hitter for those looking to maximize rewards on UPI.

If you are confused about which Super Money Credit Card belongs in your wallet (SuperCard vs SuperCard Pro), this guide will help you pick the right one. But, if you were here just for the super money credit card referral link (working as of July, 2026) then I have shared the same below. Let’s get started!

Disclaimer: This blog may contain affiliate/referral links, which may earn us a commission at no additional cost to you. These rewards helps us maintain the website but doesn’t affect our review.

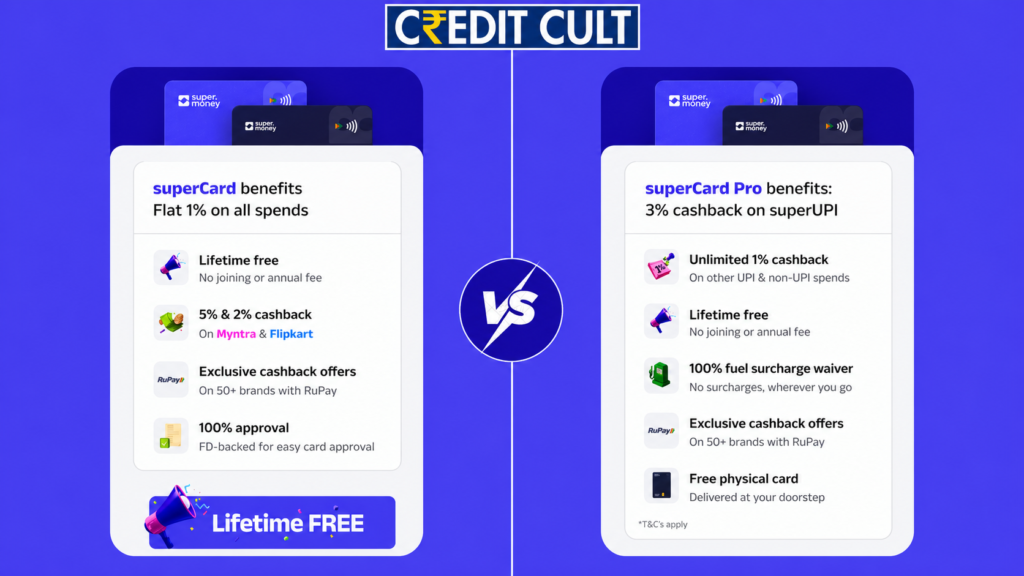

The primary difference between these two is its Reward Structure & Eligibility Requirements. While the standard SuperCard focuses on accessibility and building credit, the Pro version is designed to reward high-UPI spenders.

For better clarity, here is a head-to-head comparison of both the Super Money Credit Card Variants: SuperCard vs SuperCard Pro.

Features

SuperCard (Basic)

SuperCard Pro

Card Look

Annual Fee

Lifetime Free (LTF)

Lifetime Free (LTF)

UPI Cashback

1% Cashback

3% Cashback*

Minimum Txn Amount for Cashback

₹100

₹100

Cashback Offered

5% and 2% Cashback on Myntra & Flipkart

1% Cashback on Other UPI & Non-UPI Spends (Unlimited)

Eligibility

Good Credit Score

FD-backed

Best For

Beginners with no Credit Score

UPI Spenders

3% Cashback*: The SuperCard Pro used to offer flat 3% cashback up to ₹500/month but after the recent devaluation (in Jan’26), Axis Bank made their simple cashback rule complex. Now, cardholders can simply earn 3% Cashback up to ₹100 but after that the 3% Category Cashback can not exceed the Cashback earned through the 1% Category.

Applying for any of the Super Money Credit Card Variant is super easy. Just follow the detailed process shared below:

Download Super.Money App: Download the app with our Super Money Credit Card Referral Link to get up to ₹500 cashback on applying for the SuperCard Pro within 25 days of signup. You will also earn up to ₹100 cashback on first UPI with the app.

Provide Details & Link Bank: Signup with personal details and link your bank account with the app to start the UPI transactions.

Apply for Super Money Card: Tap on the Card Section (below), click on GET SUPERCARD PRO to get started.

Provide Income & PAN Details: Next, it will ask for PAN, Employment type and Monthly Income. Provide all that it will run the eligibility check. If you are eligible for the SuperCard Pro then it will continue for the Aadhar and Video KYC.

SuperCard (Basic Variant): But if you were found ineligible for the SuperCard Pro, it will you ask to apply for the SuperCard (basic variant). You can apply for it with any FD amount starting ₹100.

Cult Tip: Make sure to do first UPI transaction with a bigger amount to get better cashback on first UPI payment.

Why You Should Apply in 2026?

The credit landscape has shifted from “Physical Swipes” to “Digital Scans.” Here is why these cards are currently top-tier:

UPI Power: Both cards run on the RuPay network, meaning you can link them to any UPI app (BHIM, PhonePe, Google Pay, or the super.money app).

Zero Maintenance: With Lifetime Free (LTF) status, there is no pressure to spend a certain amount just to waive an annual fee.

Instant Gratification: The super.money app provides a “Super Jackpot” and instant cashback notifications, making the reward system transparent and engaging.

Ecosystem Synergy: If you shop on Flipkart or Myntra, the integration provides faster checkouts and exclusive “Super” discounts or cashbacks.

The Competition: Who Else is in the Ring?

While the SuperCard duo is strong, 2026 has brought several formidable competitors to the Indian market:

Kiwi RuPay Card: A pure-play UPI credit card that offers up to 5% Value back in form of “Kiwi” rewards for every scan, directly competing with the SuperCard Pro’s value proposition.

Tata Neu Infinity: Offering 5% back on Tata brands and 1.5% value back on UPI in form of NeuCoins. It’s a direct rival to SuperCard Pro for brand-loyal shoppers.

Note: There are many other RuPay-UPI Competitors but I consider them as the best alternative to Super Money Credit Cards.

Final Verdict: Which one for you?

Choosing the right super money credit card variant depends entirely on your need.

Apply for the SuperCard if you are building your credit from scratch or want a safe, FD-backed limit.

Apply for the SuperCard Pro if you have an existing credit history and want the highest possible cashback on your daily UPI scans.

Expert Tip: In 2026, the best strategy is to use the SuperCard Pro for all UPI transactions under ₹2,000 and keep a dedicated online card (like SBI Cashback Credit Card) for larger e-commerce purchases.

Saurabh | Founder & Content Writer at CreditCult.in

For the last 7 years, I’ve been obsessed with the Indian credit ecosystem—testing cards, deconstructing reward programs, and finding the tiny loopholes banks don’t want you to see. I don’t just write about these accounts; I use them daily to ensure the advice I give is backed by real-world results.

Yes, based on your repayment history and spending patterns, the super.money app may offer an “Upgrade to Pro” notification. This usually comes with an increased credit limit.

Is there any joining fees with Super Money Credit Card?

Currently, both cards are being offered as Lifetime Free.

Does the FD-backed SuperCard help us build Credit Score?

Yes, like any other credit card the SuperCard Pro will affect your credit score. And for the beginners that’s the best way to start your credit journey.

Is the Super Money Cashback real money?

Yes, the cashback offered by Super Money Credit Cards is real money withdrawable to bank account through UPI once you have reached the minimum cashback of ₹10.

What is the minimum cashback amount required to redeem the cashback into bank?

You have accumulate at least ₹10 cashback to request bank withdrawal.

What is the minimum FD Amount for SuperCard?

The minimum deposit required for the application journey is just ₹100.

What is the maximum cashback per month?

SuperCard offers 1% cashback on UPI and Non-UPI payments with monthly cashback limit:

Cashback on UPI transactions are capped at Rs 500 per statement month.

Cashback on non-UPI transactions are capped at Rs 10,000 per statement month.

What is the minimum transaction amount eligible for cashbacks?

Cashback is only applicable on transactions where transaction amount is greater than or equal to ₹100.

What would be the interest rate if I withdraw deposit before maturity date?

If you withdraw your deposit before the maturity date, you will lose out on interest.

Can I make a transaction bigger than

If you withdraw your deposit before the maturity date, you will lose out on interest.

How much credit limit will be issued for SuperCard (FD Based)?

It depends upon your bureau score but generally its around 90% of the total fixed deposit/s.

Is there any fees on SuperCard Physical Delivery?

Yes, delivery of Physical SuperCard costs ₹249 plus GST or get it for free by maintaining the minimum eligible fixed deposit amount (generally, ₹5,000).

Join Our Channel

Join Our Channel