Kotak 811 Super Account Personal Review | 5% Super Cashback Card

Annual Fees:

₹499/year

Benefits:

Zero Balance, 5% Cashback

Best for:

All (Casual Users)

Reward Type:

Super Cashback (100% Value)

Rating:

Kotak 811’s Zero Balance Savings Account has long been a go-to choice for Indians seeking a reliable digital savings account. Moreover, Kotak 811’s Super Savings Account makes it more attractive by offering 5% cashback on Super Debit Card Spends.

If you are wondering whether to stick to the standard zero-balance (classic) account or apply for the fee-based Kotak 811 Super Variant, this data-backed, comprehensive personal review breaks down the fees, true cashback mechanics, secret tips, and ultimate value proposition.

Let’s dive in and see if this is the right option to park your money. Don’t forget to checkout the two secret tricks at the end: How I consistently claim 5% cashback with my Super Debit Card and How I got the ₹499 joining fee returned.

About Kotak 811 Super Account

The Kotak 811 Super Account is a digital savings account customized for individuals who want the ease of zero-balance banking but also desire premium rewards on their debit card spends.

Unlike the standard lifetime-free Classic Variant, the Super account comes with a ₹499 per year subscription fee, and offers cardholders a premium VISA Platinum Debit Card, enhanced transaction limits, exclusive perks, and 5% Super Cashback.

Key Specifications At a Glance

| Feature | Details |

| Minimum Balance Requirement | Zero (No Monthly Average Balance penalty) |

| Super Program Fee | ₹499 per year |

| Primary Benefit | Flat 5% Cashback on eligible debit card spends |

| Maximum Cashback Cap | ₹500 per month (Up to ₹6,000 per year) |

| Initial Funding Required | ₹10,000 (at onboarding) |

Debit Card Spending Limits | ₹1 Lakh daily withdrawal / ₹3 Lakhs daily online purchase |

Kotak 811 Super | The 5% Cashback Super Card

While flat 5% cashback sounds like a premium credit card perk, the bank offers it with a nominal annual fee and a simple threshold to activate it. If you do not meet the criteria, you earn zero cashback.

1. The Activation Threshold (The ₹10k Rule)

Though technically Kotak 811 Super Savings Account is a zero-balance account but to trigger the cashback mechanism for any given month, you must deposit at least ₹10,000 into the super account as a single transaction during that calendar month.

Eligible Credits: UPI Deposit/Transfer, Salary credits, self-transfers from non-Kotak bank accounts, transfers from friends, or mutual fund redemption proceeds, etc.

Ineligible Credits: Bank-induced credits, transaction refunds/reversals, or Auto-Sweep (ActivMoney) inflows.

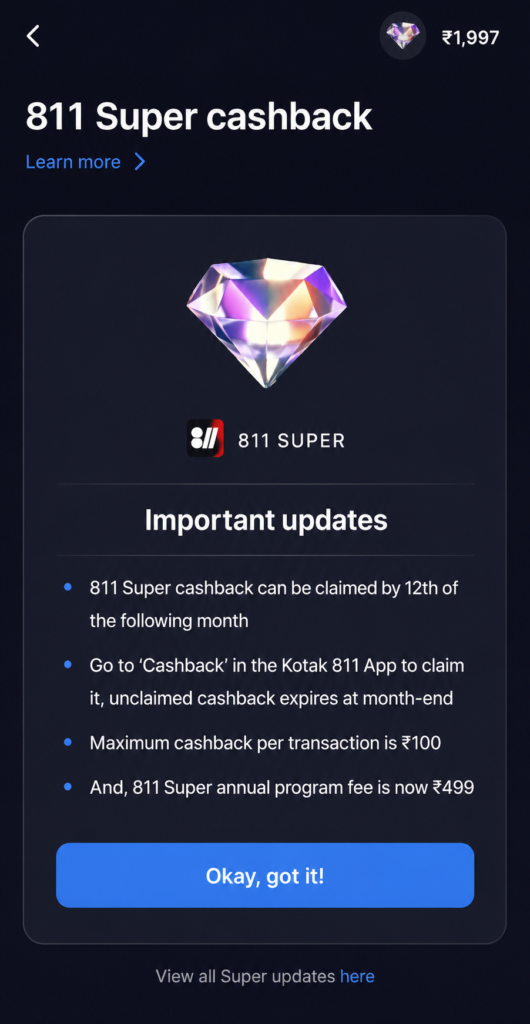

2. The “Manual Claim” Rule

Cashback does not auto-credit to your bank account.

- It comes as an unclaimed cashback in the app and

- becomes available by the 12th of the following month,

- and should be claimed by the end of the next month or the reward will expire.

3. Eligible vs. Ineligible Spending

Once activated, the 5% cashback applies to

- all eligible spends whether Online or Offline,

- using the physical or virtual 811 Super Debit Card.

Kotak 811 Super Debit Card 5% Cashback Exclusions

- 5169, 5085, 5199, 2842, 5122, 5039, 5198, 7375, 5051, 5021, 5046, 5099, 7395, 8734, 5044, 5074, 2791- Business-to-business transactions

- 7995- Betting including lottery tickets, casino gaming chips, race tracks

- 7273- Dating and escort services

- 5960- Direct marketing – Insurance services

- 6012- Financial Institution – Merchandise Services & Debt Repayment

- 7800- Government licensed – lottery

- 7801- Government licensed- online gambling

- 6381- Insurance

- 6300- Insurance sales, underwriting & premiums

- 6010- Manual cash disbursements – Financial Institutions

- 4829- Money transfer

- 6051- Non financial institutions – Foreign currency liquid, crypto assets, account funding, traveler cheques & debt repayment

- 8651- Political donations

- 6540- Non-Financial Institutions – Stored Value Card Purchase/Load

- 5300- Wholesale clubs, and 5723- Guns and ammunition shops

Trick to Save the Kotak 811 Super Program Fee

No doubt that even with a subscription fee of ₹499 the Kotak 811’s Super Savings Account is still worth it. But what if you could save on the initial joining fee?

It’s not a trick—I’m sharing a cashback opportunity! A cashback site is currently offering ₹499 Cashback (credited to your bank account within 7-30 days) when you successfully open a Kotak 811 Super Account (after initial funding of ₹10,000, and Video KYC).

Steps to Claim the ₹499 Cashback

- Visit the Cashback Site.

- Provide the site with your mobile number (used for the application) and/or your UPI ID for tracking purposes.

- You will then be redirected to the Kotak Bank website, where you can create your account as usual.

- Complete the signup process with initial funding of ₹10,000 and Video KYC.

- You should received the cashback within 7-30 days.

Disclaimer: I can’t guarantee cashback as I’m just sharing a cashback site that has worked 2 out of 3 times for me. So, please connect with them in case you don’t receive the cashback. You may also share your cashback experience for others in the comments.

Suggestion: Sign up through the cashback site only if you were already planning to open a Kotak 811 Super Account. Please don’t open an account just for the cashback.

Best Ways to Claim 5% Cashback with 811 Super

A zero balance savings account along with the 5% cashback benefit is rare. But what are the best ways to claim the cashback with Kotak 811 Super Debit Card?

Sharing below how Netizens and I am claiming the full super cashback each month. Kotak 811 Super Cashback Tricks:

- Fuel Expense: If you don’t have any credit card providing better cashback on fuel spends then Kotak 811 super debit card is one of the simple ways to earn 5% cashback that too without any fuel surcharge fee on it.

- Offline Shopping: There are very limited credit/debit cards that offer more than 1% cashback on offline spends at departmental stores, pharmacies, fashion stores, etc. While Kotak 811 Super Debit Card offers straight 5% cashback on offline spends.

- Recharge/Bill Payments: Netizens have shared that the normal recharge/bill payments through Amazon, with the Kotak 811 Super debit card, are giving them 5% cashback.

- Gift Card/Vouchers: You can claim 5% cashback even for gift card or voucher purchases through amazon or similar apps.

Amazon Pay Trick (Super Safe): Buy Amazon Pay Physical Gift Cards from the Zepto App with Kotak 811 Super Debit Card and claim 5% Cashback up to ₹500/month with it. Use the Amazon Pay Balance for Bills/Recharge/Insurance. (Verified on May, 2026)

Final Verdict: Who Should Apply for Kotak 811 Super?

Considering all the features & benefits of the Super Variant, plus, the ₹499 Cashback Offer the Kotak 811 Super Variant is highly recommendable and worth signing up for.

Apply If:

- You frequently shop online or offline at fashion stores, departmental stores, fuel stations and lack a good cashback card for any of them.

- You can easily deposit ₹10,000 in a single transaction and can easily spend at least ₹1,000 per month to recover the Kotak 811 Super Program Fee.

Skip If:

- You have better cashback card alternatives especially for offline spends.

- You want a completely Life time free zero balance savings account. In such case, you can apply for the Kotak 811 Classic Variant.

Saurabh | Founder & Content Writer at CreditCult.in

For the last 7 years, I’ve been obsessed with the Indian credit ecosystem—testing cards, deconstructing reward programs, and finding the tiny loopholes banks don’t want you to see. I don’t just write about these accounts; I use them daily to ensure the advice I give is backed by real-world results.

I believe you found this post useful. I would also recommend you to read out our latest blog on Slice Bank Account and Credit Card.

How to Open Kotak 811 Super Account?

Opening Kotak 811 Savings Account is a quick and fully digital process. I have shared the detailed steps to open Kotak 811 account below:

- Visit Kotak 811 Website.

- Enter your Mobile Number, Email ID and Pin Code to get started. Next, verify your mobile number with OTP.

- Enter your PAN and Aadhar details in the next step and then verify Aadhar via OTP.

- On the next page, share your personal details like: Father’s Name, Occupation, etc

- They will retrieve your address in the next step, just confirm it.

- On the next page, they will ask your communication address. You can click on same as Permanent Address or put different details, if not same.

- Next, give nominee details and then agree with their terms and conditions.

- Finally, they will ask the required Kotak 811 Variant: Super or Classic. (Suggestion: Choose Super for 5% Cashback and Superior Banking Experience)

- Next, you have to fund your account: ₹10,000 for Super or ₹2,500 for Classic Variant. (Using UPI)

- Once funded, you have to setup MPIN for the app and banking and then can complete the KYC process with Video KYC or Schedule Appointment (Home).

- Next, you should download the Kotak 811 app and start using the app.

Cult Tip: Kotak 811 might advertise their Video KYC service to be 24/7 available, but for me, Video KYC option was not enabled at night, near 23:40. So, maybe Video KYC option is available between normal working hours: 9:00 to 19:00 IST.

Kotak 811 Super Account: Key Features & Benefits

- Instant Digital Account: Open an account within minutes with your convenience from your home with just your Aadhaar and PAN details.

- Zero Balance: No requirement for maintaining a minimum balance.

- Virtual Debit Card: Get an instant virtual debit card within the app for online payments.

- Physical Debit Card: Option to request a physical card (for free) through the app for ATM use and POS transactions.

- Mobile Banking: Manage everything through the Kotak 811 Mobile App.

- Interest & Rewards: Earn interest on savings balance and 5% rewards.

- Free Fund Transfers: Utilize NEFT, IMPS, and RTGS for online fund transfers at no cost.

- 811 Super Program Fee: Kotak 811 Super Account costs ₹499 annually but above I have already shared a trick to save on program fees.

- 5% Super Cashback: Get 5% cashback up to ₹500/month on eligible spends with the Super Variant.

Saurabh | Founder & Content Writer at CreditCult.in

For the last 7 years, I’ve been obsessed with the Indian credit ecosystem—testing cards, deconstructing reward programs, and finding the tiny loopholes banks don’t want you to see. I don’t just write about these accounts; I use them daily to ensure the advice I give is backed by real-world results.

I believe you found this post useful. I would also recommend you to read out our latest blog on Slice Bank Account and Credit Card.

Pingback: Multipl Referral Code 6G7WX | Get 250 Signup Bonus - Credit Cult